Noticed “POD” on your bank statement and wondering what it means? This three-letter abbreviation can be confusing, especially since it has multiple meanings in the banking and financial world. Whether you’re reviewing your account details, setting up estate planning, or simply trying to understand your statement better, this comprehensive guide explains everything you need to know about POD and what it means for your finances.

What Does POD Mean on a Bank Statement?

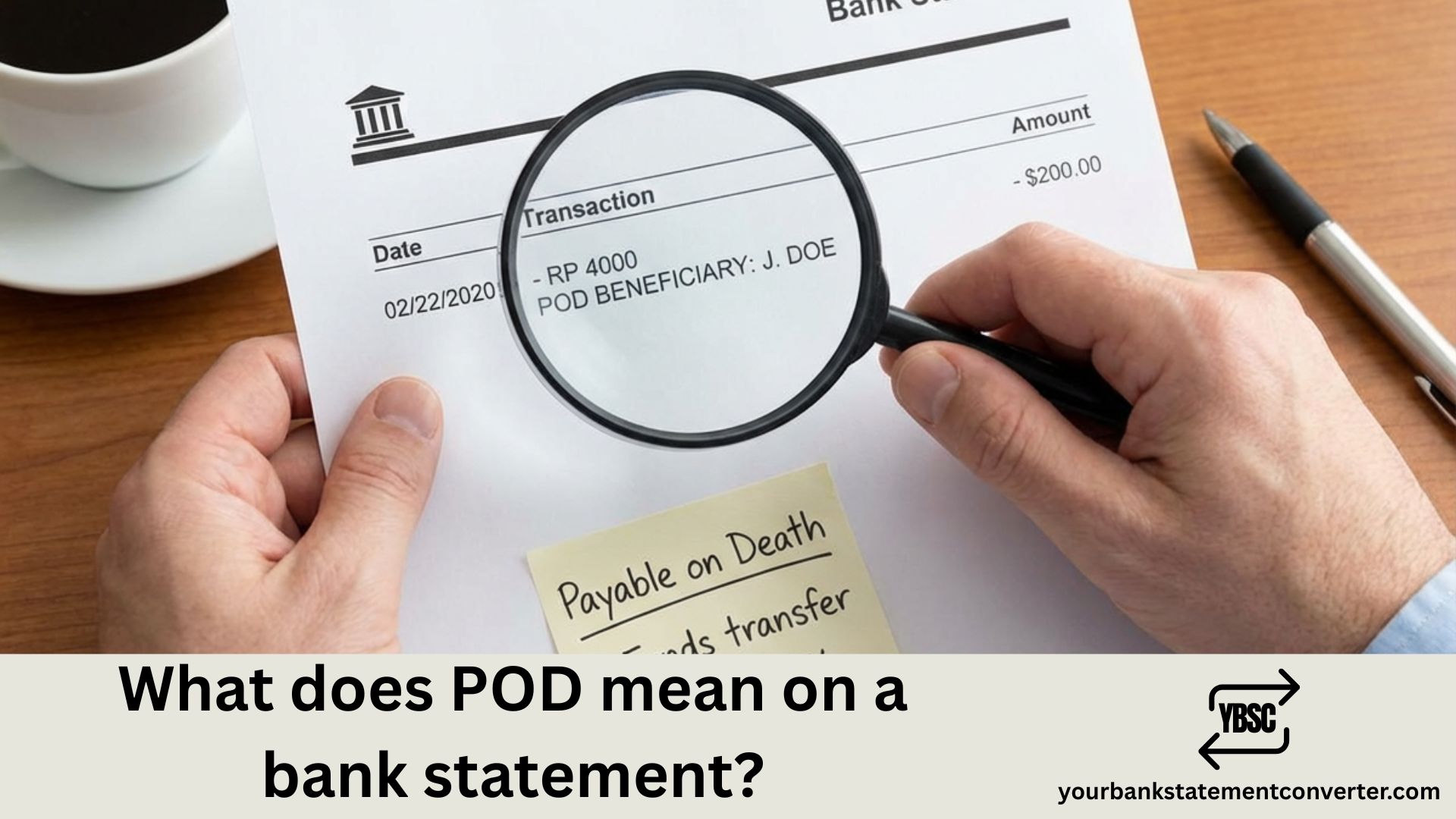

POD on a bank statement most commonly stands for Payable on Death, which indicates that your bank account has a designated beneficiary who will receive the funds when you pass away. When you see “POD” followed by a name on your statement—such as “POD: John Smith”—it means John Smith is designated to inherit the account balance upon your death.

However, POD can have other meanings in banking and finance contexts:

Primary Meanings of POD:

| Abbreviation | Full Term | Context |

|---|---|---|

| POD | Payable on Death | Estate planning, account beneficiary designation |

| POD | Proof of Deposit | Check processing, deposit verification |

| POD | Proof of Delivery | Transactions, shipping confirmations |

| POD | Pay on Delivery | Payment terms for goods/services |

The most common usage on personal bank statements is Payable on Death, which is an important estate planning tool that allows your money to transfer directly to your beneficiaries without going through probate court.

Understanding Payable on Death (POD) Accounts

A Payable on Death account is a bank account that automatically transfers to your designated beneficiary when you die. It’s sometimes called a “Totten Trust,” “bank account trust,” or informally known as a “poor man’s trust” because it accomplishes similar goals to more expensive legal instruments without attorney fees.

How POD Accounts Work:

- During your lifetime: You maintain complete control over the account. You can deposit, withdraw, close the account, or change beneficiaries at any time. The beneficiary has no rights to the money while you’re alive.

- Upon your death: The funds automatically transfer to your named beneficiary outside of probate court. The beneficiary simply needs to provide a certified death certificate and valid identification to claim the funds.

- Multiple beneficiaries: You can name multiple POD beneficiaries, and the funds will typically be split equally unless you specify different percentages.

Key Characteristics of POD Accounts:

- No cost to set up at most financial institutions

- Available for checking accounts, savings accounts, money market accounts, and CDs

- Beneficiary designation overrides instructions in your will

- Funds bypass probate, providing quick access to money

- Can increase your FDIC insurance coverage (each beneficiary adds $250,000 coverage)

Why POD Appears on Your Bank Statement

If you see POD on your bank statement, it’s there for one of these reasons:

1. You Set Up a Beneficiary Designation

When you opened your account or later added a beneficiary, the bank recorded this designation. The POD notation confirms that someone will inherit the account upon your death.

2. New Account Setup Confirmation

Banks often display POD information on initial statements after you’ve completed beneficiary paperwork, confirming the designation is active.

3. Beneficiary Update

If you recently changed or added a beneficiary, the POD notation may appear or update on your next statement.

4. Bank’s Standard Formatting

Some banks consistently display POD information on every statement as a reminder of your beneficiary designation, while others only show it periodically.

What the POD Entry Typically Looks Like:

- POD: Jane Doe

- POD Beneficiary: John Smith

- Acct Type: Savings POD

- POD (50%): Sarah Johnson, POD (50%): Michael Johnson

POD vs. Joint Account vs. Trust: What’s the Difference?

Understanding how POD accounts compare to other account types helps you make informed decisions about your finances:

POD Account:

- You have sole control during your lifetime

- Beneficiary has no access until your death

- Simple to set up with no legal fees

- Bypasses probate

- Can name any person or charity as beneficiary

Joint Account:

- Both parties have full access while alive

- Surviving owner automatically inherits

- Risk: Joint owner can withdraw all funds at any time

- Doesn’t require death certificate to access

Trust Account:

- Most complex and expensive to establish

- Offers greater control over how money is distributed

- Can include conditions on inheritance

- Protects assets during incapacity

- Bypasses probate

For most people, a POD designation offers the best balance of simplicity, cost (free), and effectiveness for transferring bank accounts to heirs.

Managing Multiple Bank Accounts and POD Designations?

Keeping track of POD designations, beneficiaries, and account details across multiple banks can be challenging—especially when your statements come in different formats and layouts.

Your Bank Statement Converter helps accountants, bookkeepers, estate planners, and individuals organize their financial data by converting PDF bank statements into clear, editable formats.

How Your Bank Statement Converter helps with estate and financial planning:

- ✅ Convert statements from all major banks to Excel, CSV, or QBO

- ✅ Easily compile account information for beneficiary reviews

- ✅ Create organized records for estate planning documentation

- ✅ Track multiple accounts across different institutions

- ✅ Simplify account reconciliation and financial audits

Whether you’re managing your own finances or handling estate administration for a loved one, having your bank data in an organized, searchable format makes everything easier.

Convert Your Bank Statements Today →

How to Set Up a POD Beneficiary on Your Bank Account

Adding a POD designation to your bank account is straightforward and typically free:

Step 1: Contact Your Bank Call, visit a branch, or log into your online banking to request a POD or beneficiary designation form.

Step 2: Gather Beneficiary Information You’ll need each beneficiary’s:

- Full legal name

- Date of birth

- Current address

- Phone number

- Social Security number (some banks require this)

Step 3: Complete the Form Fill out the form specifying:

- Which account(s) the POD applies to

- Beneficiary name(s) and contact information

- Percentage split (if multiple beneficiaries)

- Contingent beneficiaries (optional backup beneficiaries)

Step 4: Submit and Confirm Return the form to your bank and request confirmation that the POD designation is active. Check your next statement to verify the POD notation appears.

How Beneficiaries Claim POD Account Funds

When an account holder passes away, the POD beneficiary can claim the funds with minimal hassle:

Documents Needed:

- Certified copy of the death certificate (obtain 2-3 copies)

- Valid government-issued ID (driver’s license or passport)

- Proof of POD designation (account statement showing POD or bank records)

Process:

- Contact the bank (call ahead to schedule an appointment)

- Present death certificate and identification

- Complete any required bank forms

- Receive funds via check, transfer, or new account

Timeline: Most banks release POD funds within a few days to a couple of weeks after receiving proper documentation. Some states may have a short waiting period (typically 10-30 days).

Important Considerations for POD Accounts

Before setting up or relying on POD accounts, consider these factors:

Advantages:

- Avoids probate court delays and costs

- Quick access to funds for funeral expenses and bills

- Simple and free to establish

- Easy to change beneficiaries

- Increases FDIC insurance coverage

- Maintains privacy (unlike probate, which is public record)

Limitations:

- Cannot restrict how beneficiary uses the funds

- Doesn’t help during your lifetime incapacity

- May conflict with overall estate plan if not coordinated

- No contingent beneficiaries at some banks

- Creditors may still have claims against POD accounts

- If beneficiary predeceases you, funds may go to probate

Best Practices:

- Keep beneficiary designations current (especially after marriage, divorce, or death of a beneficiary)

- Coordinate POD designations with your will and overall estate plan

- Name contingent beneficiaries when possible

- Review and update periodically

- Inform beneficiaries about the accounts

Other Meanings of POD in Banking

While Payable on Death is the most common meaning on personal bank statements, POD has other applications:

Proof of Deposit (POD): In check processing, POD refers to verifying that the dollar amount on a check matches the deposit slip. This is part of the bank’s internal verification process and typically doesn’t appear on customer statements.

Proof of Delivery: In transaction records, particularly for online purchases or business accounts, POD may indicate that delivery of goods or services has been confirmed. This might appear on business banking statements alongside transaction descriptions.

Pay on Delivery: Also known as “Cash on Delivery” (COD), this payment term means payment is due when goods are delivered. Businesses may see this notation on commercial banking statements.

Understanding POD on Your Bank Statement: Key Takeaways

POD on your bank statement typically means “Payable on Death,” indicating you’ve designated a beneficiary for your account. This simple designation is a powerful estate planning tool that ensures your money goes directly to your chosen beneficiaries without the delays and costs of probate court.

Understanding your bank statement—including notations like POD—is essential for effective financial management and estate planning. Whether you’re setting up beneficiaries for the first time, reviewing an inherited account, or managing finances for yourself or clients, having clear visibility into your banking information is crucial.

For professionals managing multiple accounts or handling estate administration, Your Bank Statement Converter transforms complex PDF statements into organized, actionable data—making it easy to track account details, verify beneficiary information, and maintain accurate financial records.

Frequently Asked Questions (FAQs)

What does POD mean on a bank statement?

POD on a bank statement stands for “Payable on Death,” which indicates the account has a designated beneficiary who will receive the funds when the account holder passes away. The beneficiary’s name typically appears after the POD designation, such as “POD: Jane Doe.”

Is a POD account the same as a beneficiary?

Yes, essentially. A POD designation is the method by which you name a beneficiary for your bank account. When you set up a POD account, you’re designating who will receive the money upon your death. The terms “POD beneficiary” and “account beneficiary” are often used interchangeably.

Does POD override a will?

Yes, in most cases a POD designation overrides any conflicting instructions in your will. POD accounts are considered “non-probate assets,” meaning they transfer directly to the named beneficiary regardless of what your will states. This is why it’s important to keep your POD designations consistent with your overall estate plan.

Can I have multiple POD beneficiaries?

Yes, most banks allow you to name multiple POD beneficiaries. Unless you specify otherwise, the funds will typically be divided equally among all named beneficiaries. Some banks allow you to designate specific percentages for each beneficiary.

What happens to a POD account if the beneficiary dies first?

If your POD beneficiary passes away before you do, the account typically reverts to your estate and may go through probate (unless you have other beneficiaries named). This is why it’s important to name contingent (backup) beneficiaries when possible and regularly review your designations.

Does a POD beneficiary have access to the account while I’m alive?

No, a POD beneficiary has absolutely no rights to access the account while you’re alive. You maintain complete control—you can withdraw all the money, close the account, or change the beneficiary at any time without the beneficiary’s knowledge or consent.

How does a POD beneficiary claim the money after death?

To claim POD funds, the beneficiary must present a certified copy of the death certificate and valid government-issued identification to the bank. The bank will verify the POD designation on file and release the funds, typically within a few days to a couple of weeks.

Is there a fee to set up a POD on my bank account?

No, most banks offer POD designation at no cost. It’s a free service that simply requires filling out a beneficiary designation form. There are no ongoing fees or charges associated with maintaining a POD designation.

What’s the difference between POD and TOD?

POD (Payable on Death) and TOD (Transfer on Death) serve the same purpose but apply to different asset types. POD is typically used for bank accounts, while TOD is used for investment accounts, brokerage accounts, and in some states, real estate. Both allow assets to transfer to beneficiaries outside of probate.

Can creditors claim money from a POD account after death?

Yes, in some cases creditors can still make claims against POD accounts if the deceased had outstanding debts. While POD accounts bypass probate, they may still be subject to creditor claims depending on state law and the nature of the debts. The beneficiary should not assume POD funds are protected from all creditor claims.

Disclaimer: This article is for informational purposes only and does not constitute legal, financial, or estate planning advice. Laws regarding POD accounts vary by state. Consult with a qualified attorney or financial advisor for guidance specific to your situation.