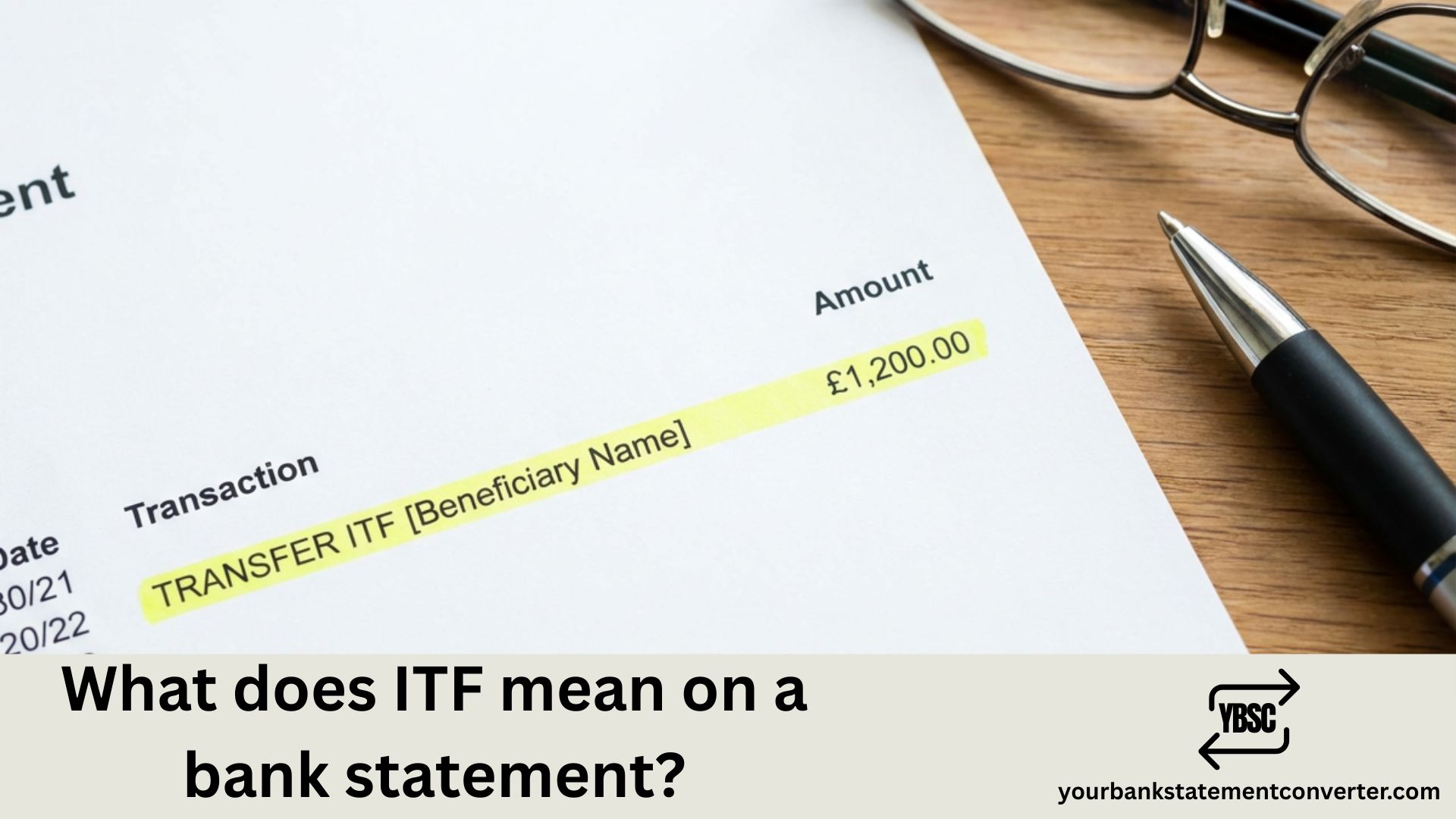

If you’ve noticed “ITF” on your bank statement and wondered what it means, you’re not alone. This banking abbreviation appears on millions of accounts worldwide—and understanding it is essential for estate planning, managing family finances, and maximizing your FDIC insurance coverage.

This guide explains exactly what ITF means, how these accounts work, and when you might want to use one.

What Does ITF Mean on a Bank Statement? [Quick Answer]

ITF stands for “In Trust For.” When you see ITF on a bank statement, it indicates the account is held by one person (the trustee) for the benefit of another person (the beneficiary).

ITF accounts are a type of informal trust account—also known as:

- Totten Trust

- POD (Payable on Death) Account

- ATF (As Trustee For) Account

- TOD (Transfer on Death) Account

These accounts allow the account owner to maintain full control of the funds during their lifetime while designating who will receive the money after they pass away—without going through probate.

How ITF Accounts Work

An ITF account creates a simple trust arrangement between three parties:

| Role | Description |

|---|---|

| Account Owner / Trustee | The person who opens and controls the account |

| Beneficiary | The person who will receive the funds upon the owner’s death |

| Financial Institution | The bank or credit union holding the account |

Key Features of ITF Accounts

- Owner maintains full control — You can deposit, withdraw, and close the account at any time during your lifetime.

- Beneficiary has no access until death — The named beneficiary cannot touch the funds while you’re alive.

- Bypasses probate — Funds transfer directly to the beneficiary upon your death, avoiding the lengthy probate process.

- Revocable — You can change or remove the beneficiary at any time without their consent.

- Easy to set up — Simply complete the bank’s beneficiary designation form; no attorney required.

ITF vs. POD: What’s the Difference?

While ITF and POD are often used interchangeably, there are subtle differences:

| Feature | ITF (In Trust For) | POD (Payable on Death) |

|---|---|---|

| Structure | Implies a trust relationship | Simple beneficiary designation |

| Trustee role | Account holder acts as trustee | No formal trustee role |

| During lifetime | Trustee holds funds for beneficiary | Owner owns funds outright |

| Beneficiary rights | May have equitable ownership | No rights until owner’s death |

| Asset protection | Potentially better creditor protection | Less asset protection |

| Probate avoidance | Yes | Yes |

Bottom Line: Both achieve the same goal—transferring funds to a beneficiary outside of probate. The terms are often used interchangeably by banks, though ITF implies a slightly more formal trust arrangement.

Common Uses for ITF Accounts

1. Saving for Children or Grandchildren

Parents and grandparents frequently open ITF accounts to:

- Set aside money for a child’s education

- Save for a future car purchase

- Build a nest egg that transfers at a specific age

- Keep funds managed by a responsible adult until the child matures

Example: Grandma opens a savings account “Jane Smith ITF Tommy Smith” to save for Tommy’s college education. Jane controls the funds until her death or until she decides to transfer them to Tommy.

2. Simple Estate Planning

ITF accounts offer a straightforward way to pass assets to loved ones without:

- Creating a formal trust (which requires legal fees)

- Going through probate (which can be expensive and time-consuming)

- Updating your will

3. Protecting Assets from Probate

Assets in ITF accounts transfer directly to the named beneficiary upon the account holder’s death. This means:

- Faster access to funds for beneficiaries

- No court involvement or probate fees

- Privacy (probate records are public)

4. Maximizing FDIC Insurance Coverage

ITF accounts qualify for separate FDIC insurance coverage in the “Trust Accounts” category, which can significantly increase your protected deposits (more on this below).

FDIC Insurance for ITF Accounts

Understanding how FDIC insurance applies to ITF accounts can help you protect more of your money.

Current FDIC Rules (Effective April 1, 2024)

ITF accounts are classified as revocable trust accounts for FDIC insurance purposes. Coverage is calculated as:

$250,000 × Number of Eligible Beneficiaries = Total Coverage (Maximum: $1,250,000 per owner if 5+ beneficiaries)

FDIC Coverage Examples

| Scenario | Coverage Amount |

|---|---|

| ITF account with 1 beneficiary | $250,000 |

| ITF account with 2 beneficiaries | $500,000 |

| ITF account with 3 beneficiaries | $750,000 |

| ITF account with 5+ beneficiaries | $1,250,000 (maximum) |

Important Notes

- Beneficiaries must be named in the bank’s records for coverage to apply

- Only living people and IRS-recognized charities count as eligible beneficiaries

- All trust accounts (ITF, POD, formal trusts) at the same bank are combined for insurance limits

- Coverage is per owner, per beneficiary, per bank

Pro Tip: If you have significant deposits, strategically using ITF accounts with multiple beneficiaries can increase your total FDIC coverage beyond the standard $250,000.

How to Set Up an ITF Account

Setting up an ITF account is straightforward:

- Visit your bank or log into online banking

- Request to add a beneficiary to your existing account, or open a new account with an ITF designation

- Complete the beneficiary designation form with the beneficiary’s full legal name, date of birth, and Social Security number

- Review and confirm the designation is recorded correctly

Required Information

- Beneficiary’s full legal name

- Date of birth

- Social Security number (usually required)

- Relationship to account holder

- Percentage share (if multiple beneficiaries)

How to Change or Remove an ITF Beneficiary

Because ITF accounts are revocable, you can modify beneficiaries at any time:

- Contact your bank or log into online banking

- Request to change the beneficiary designation

- Complete the updated form

- Confirm the bank has updated their records

Important: Instructions in your will do not override ITF beneficiary designations. If your will says your son should inherit the account but your ITF designation names your daughter, your daughter receives the funds.

What Happens When the Account Holder Dies?

When an ITF account holder passes away:

- Beneficiary contacts the bank with a certified death certificate

- Bank verifies the death and beneficiary identity

- Funds transfer directly to the beneficiary (no probate required)

- Beneficiary receives the money usually within days to a few weeks

Multiple Beneficiaries

If multiple beneficiaries are named, funds are typically split equally unless the account owner specified different percentages.

ITF Account Advantages and Disadvantages

Advantages

✅ Avoids probate — Faster, cheaper transfer of assets

✅ Easy to set up — No attorney or formal trust document needed

✅ Maintains control — Owner keeps full access during lifetime

✅ Revocable — Can change beneficiaries anytime

✅ Increases FDIC coverage — Each beneficiary adds $250,000 coverage

✅ Privacy — Avoids public probate records

Disadvantages

❌ Overrides your will — Beneficiary designation takes precedence

❌ No conditions — Cannot set conditions like “when they turn 25”

❌ Potential for unintended consequences — Forgetting to update after divorce, death, or family changes

❌ Beneficiary gets all at once — No structured distributions

❌ Tax implications — May be subject to estate taxes (assets count toward estate value)

Organize Your ITF Account Statements with Ease

Whether you’re managing ITF accounts for estate planning, tracking deposits for beneficiaries, or preparing tax records, keeping organized financial records is essential.

YourBankStatementConverter.com makes it easy to convert your PDF bank statements into clean Excel or CSV files—perfect for tracking ITF account activity, preparing estate documentation, or sharing financial records with attorneys and accountants.

Why Financial Planners and Families Use This Tool

- Works with any bank worldwide — Chase, Bank of America, Wells Fargo, HSBC, Barclays, TD Bank, and thousands more

- AI-powered accuracy — Extracts all transaction details precisely

- Handles scanned statements — OCR technology converts image-based PDFs

- Multiple currency support — Essential for international families and estates

- Secure & encrypted — Bank-level security for sensitive financial data

- Ready for accounting software — Export to QuickBooks, Xero, or Excel

Perfect For

- Tracking deposits into children’s or grandchildren’s ITF accounts

- Preparing estate documentation for attorneys

- Organizing financial records for beneficiaries

- Creating clear transaction histories for tax purposes

👉 Try Your Bank Statement Converter Now — Upload your statements and get organized Excel data in seconds.

Other Banking Abbreviations You Should Know

| Abbreviation | Meaning | Description |

|---|---|---|

| ITF | In Trust For | Account held for beneficiary |

| POD | Payable on Death | Funds payable to beneficiary upon death |

| ATF | As Trustee For | Similar to ITF |

| TOD | Transfer on Death | Assets transfer upon death |

| JTWROS | Joint Tenants with Rights of Survivorship | Joint account passes to survivor |

| UTMA | Uniform Transfers to Minors Act | Custodial account for minors |

| UGMA | Uniform Gifts to Minors Act | Gift account for minors |

Frequently Asked Questions (FAQs)

What does ITF mean on a bank statement?

ITF stands for “In Trust For.” It indicates the account is held by one person (trustee) for the benefit of another person (beneficiary). The trustee controls the account during their lifetime, and funds transfer directly to the beneficiary upon the trustee’s death without going through probate.

Is an ITF account the same as a POD account?

They’re very similar and often used interchangeably by banks. Both allow you to name a beneficiary who receives the funds upon your death. The main difference is that ITF implies a trust relationship where the owner acts as trustee, while POD is simply a beneficiary designation. Both bypass probate.

Can the beneficiary access an ITF account while the owner is alive?

No. The beneficiary has no access to the funds until the account owner dies. The owner maintains complete control—they can withdraw money, close the account, or change the beneficiary at any time without the beneficiary’s knowledge or consent.

How do I remove someone from an ITF account?

Contact your bank and request to change the beneficiary designation. Complete the updated form, and the bank will update their records. You do not need the beneficiary’s permission to remove them since ITF accounts are revocable.

Does an ITF account avoid probate?

Yes. One of the main benefits of ITF accounts is that funds transfer directly to the named beneficiary upon the owner’s death, completely bypassing the probate process. This means faster access to funds and no court involvement.

How much FDIC insurance does an ITF account have?

ITF accounts are insured up to $250,000 per beneficiary, with a maximum of $1,250,000 per owner if five or more beneficiaries are named. For example, an ITF account with three beneficiaries would be insured up to $750,000.

Can I have multiple beneficiaries on an ITF account?

Yes. You can name multiple beneficiaries on an ITF account. Unless you specify otherwise, they will share the funds equally upon your death. Each beneficiary adds $250,000 of FDIC insurance coverage, up to the $1,250,000 maximum.

What happens to an ITF account if the beneficiary dies first?

If the beneficiary dies before the account owner, the account reverts to the owner’s estate (unless a contingent beneficiary was named). The funds would then go through probate. It’s important to update beneficiary designations when circumstances change.

Is money in an ITF account taxable?

ITF account funds are included in the owner’s estate for federal estate tax purposes. However, the beneficiary typically does not pay income tax when receiving the inherited funds. Consult a tax advisor for your specific situation.

What’s the difference between ITF and a formal trust?

An ITF account is an “informal trust” created simply by filling out a bank form. A formal trust requires a written trust agreement drafted by an attorney. Formal trusts offer more control (conditions, age restrictions, structured distributions) but cost more to set up and maintain.

Final Thoughts

ITF (In Trust For) is a simple but powerful designation that appears on bank statements when an account is held for the benefit of another person. These accounts offer an easy way to pass money to loved ones without the expense and delays of probate, while potentially increasing your FDIC insurance coverage.

Whether you’re setting up an ITF account for a child or grandchild, managing estate planning, or simply trying to understand your bank statement, knowing what ITF means helps you make informed financial decisions.

Need to organize your ITF account statements or prepare documentation for estate planning? YourBankStatementConverter.com converts PDF bank statements to Excel in seconds—trusted by families, financial planners, and estate attorneys across the USA, UK, Canada, and Australia.