If you’ve recently checked your bank statement and noticed a transaction labeled “EDI payment” or “EDI PMT,” you’re not alone. Many Americans encounter this term and wonder what it means for their finances. This comprehensive guide will explain everything you need to know about EDI payments, how they appear on bank statements, and what to do if you spot one.

What is an EDI Payment?

EDI stands for Electronic Data Interchange. An EDI payment is a digital transaction where money is transferred electronically from one bank account to another, accompanied by structured payment information that helps businesses process payments automatically.

Unlike traditional paper checks or simple wire transfers, EDI payments include detailed data about the transaction—such as invoice numbers, payment terms, and remittance information—all in a standardized electronic format.

How EDI Payments Work

When a company sends an EDI payment, they’re not just transferring money. They’re also sending a digital “message” that includes:

- Payment amount

- Invoice or reference numbers

- Payment date

- Vendor or customer identification

- Account information

- Any relevant payment terms or notes

This information flows directly into the recipient’s accounting or ERP system, eliminating the need for manual data entry and reducing errors.

Why Do EDI Payments Appear on Your Bank Statement?

EDI payments show up on your bank statement when:

- You’ve received a business payment: If you’re a vendor, freelancer, or contractor, clients may pay you via EDI

- Your employer uses EDI for payroll: Some companies process payroll through EDI systems

- Insurance reimbursements: Health insurance providers often use EDI for claims payments

- Government payments: Social Security, tax refunds, or other government disbursements may appear as EDI payments

- Automated bill payments: Some recurring bills are paid through EDI systems

Common Types of EDI Payments on Bank Statements

ACH EDI Payments (CCD+)

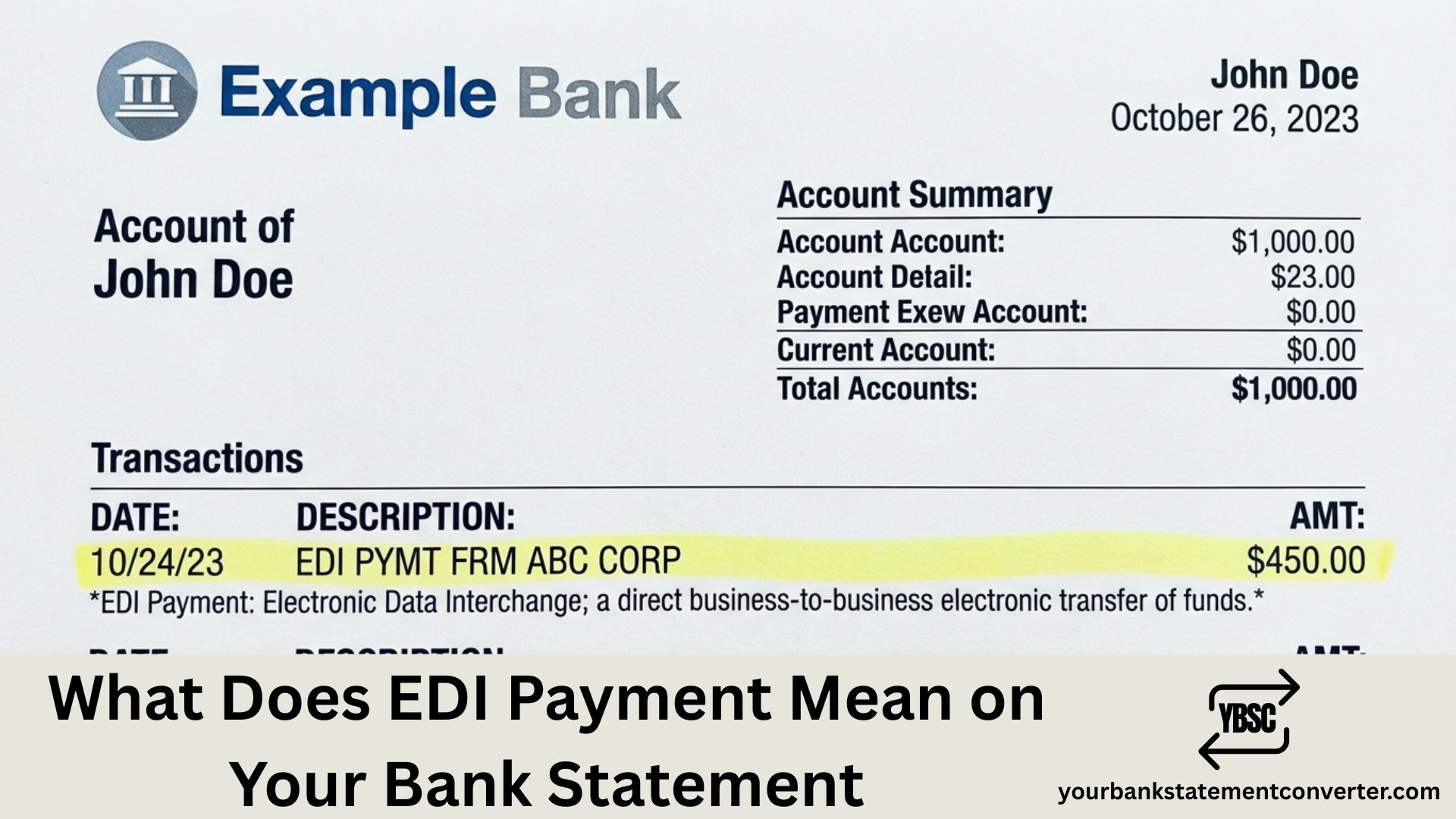

The most common type you’ll see is an ACH (Automated Clearing House) payment with EDI data, specifically called CCD+ (Cash Concentration or Disbursement Plus Addenda). These appear on your statement with transaction codes like:

- “ACH EDI PAYMENT”

- “EDI PMT”

- “ACH CCD+”

Wire Transfer EDI

Some larger transactions use wire transfers combined with EDI data, which may appear as:

- “WIRE EDI”

- “EDI WIRE TRANSFER”

Healthcare EDI Payments (835)

Medical providers often receive payments labeled:

- “EDI 835”

- “HEALTHCARE EDI”

- “EFT 835”

How to Identify EDI Payments on Your Statement

Look for these indicators:

Transaction Description: Terms like “EDI,” “EDI PMT,” “ACH EDI,” or “CCD+” in the description field

Sender Information: Usually includes the company name or abbreviated version

Reference Numbers: Often includes invoice numbers, payment IDs, or other transaction identifiers

Consistency: EDI payments from the same source typically appear with similar formatting each time

Are EDI Payments Safe?

Yes, EDI payments are generally very secure. Here’s why:

Security Features

- Encryption: Data is encrypted during transmission

- Standardization: Uses secure, regulated formats (ANSI X12, EDIFACT)

- Bank verification: Processed through regulated banking systems

- Audit trails: Complete transaction history for tracking and verification

However, Stay Vigilant

While EDI payments themselves are secure, you should still:

- Verify unexpected EDI payments with the sender

- Check that payment amounts match your invoices or expected payments

- Report any suspicious or unrecognized EDI transactions to your bank immediately

- Monitor your account regularly for unauthorized activity

What to Do When You See an Unfamiliar EDI Payment

Step 1: Check Your Records

Review your:

- Recent invoices or bills

- Pending payments from clients or employers

- Insurance claims

- Tax returns or government correspondence

Step 2: Identify the Sender

Look for:

- Company name in the transaction description

- Reference numbers that might match invoices

- Transaction amounts that align with expected payments

Step 3: Contact the Sender

If you identify the company but need clarification:

- Call their accounts payable department

- Use the reference number to inquire about the payment

- Request detailed remittance information

Step 4: Contact Your Bank

If the payment seems fraudulent or you can’t identify it:

- Call your bank’s fraud department immediately

- Provide transaction details (date, amount, description)

- Consider placing a fraud alert on your account

- File a dispute if necessary

Benefits of EDI Payments

For Businesses Receiving Payments

Faster Processing: Automated posting to accounting systems saves hours of manual work

Reduced Errors: No need to manually enter payment data from checks or emails

Better Cash Flow: Payments arrive electronically, often faster than checks

Automatic Reconciliation: Payment data matches automatically with invoices

Lower Costs: No check processing fees, less paper handling

For Payers

Improved Efficiency: Bulk payments can be processed simultaneously

Enhanced Tracking: Complete digital records of all transactions

Cost Savings: Eliminates check printing, postage, and manual processing

Better Supplier Relationships: Faster payments improve vendor relations

EDI Payment vs. Regular ACH: What’s the Difference?

| Feature | Standard ACH | EDI Payment (ACH CCD+) |

|---|---|---|

| Payment transfer | Yes | Yes |

| Remittance data | Limited or separate | Integrated with payment |

| Automation capability | Basic | Advanced |

| Invoice matching | Manual | Automatic |

| Data standardization | Basic | Comprehensive |

| Common uses | Direct deposit, bill pay | B2B payments, vendor payments |

Industries That Commonly Use EDI Payments

Healthcare

Medical providers receive EDI 835 payments from insurance companies for claims processing. These payments include detailed explanations of benefits (EOB) data.

Retail and Manufacturing

Suppliers receive EDI payments from major retailers like Walmart, Target, and Amazon for product deliveries.

Transportation and Logistics

Carriers receive EDI payments for freight services, including detailed shipment information.

Government Contractors

Vendors working with federal, state, or local governments often receive payments through EDI systems.

Professional Services

Consultants, freelancers, and service providers increasingly receive EDI payments from corporate clients.

How to Set Up Your Business to Receive EDI Payments

1. Talk to Your Bank

Most banks offer EDI-compatible business accounts. Ask about:

- ACH CCD+ capabilities

- EDI payment processing fees

- Integration with your accounting software

- Technical support for setup

2. Choose Accounting Software

Select software that supports EDI, such as:

- QuickBooks Enterprise

- SAP

- Oracle NetSuite

- Microsoft Dynamics

- Sage Intacct

3. Implement EDI Translation Software

You may need EDI translation software to:

- Convert EDI formats (ANSI X12, EDIFACT)

- Map data to your accounting system

- Validate transaction data

- Generate acknowledgments

4. Notify Your Clients

Provide your clients with:

- Your bank account information

- EDI enrollment forms

- Your preferred EDI transaction sets

- Contact information for payment issues

Understanding EDI Transaction Codes on Statements

When reviewing your bank statement, you might see various codes associated with EDI payments:

CCD (Cash Concentration or Disbursement): Basic corporate payment without addenda

CCD+ (CCD Plus Addenda): Corporate payment with additional remittance data

CTX (Corporate Trade Exchange): Complex B2B payments with extensive remittance information

PPD (Prearranged Payment and Deposit): Consumer payments, sometimes with EDI data

SEC Code: The type of ACH transaction (appears on detailed statements)

Troubleshooting Common EDI Payment Issues

Payment Amount Doesn’t Match Invoice

Possible reasons:

- Early payment discount applied

- Partial payment made

- Deductions for damaged goods or disputes

- Currency conversion (for international transactions)

Solution: Check the EDI remittance data for details about adjustments

Missing Remittance Information

Possible reasons:

- Bank doesn’t support full EDI data display

- Payer didn’t include complete data

- Technical error in transmission

Solution: Contact the payer’s accounts payable for detailed remittance

Duplicate Payments

Possible reasons:

- System error on payer’s side

- Reprocessed transaction

- Multiple invoices paid at once

Solution: Verify with the payer and return excess funds if necessary

Payment to Wrong Account

Possible reasons:

- Outdated account information

- Data entry error by payer

- Multiple accounts with similar names

Solution: Contact payer immediately and your bank to arrange transfer correction

Tax Implications of EDI Payments

EDI payments are taxable income just like any other business payment. However, they offer advantages for tax preparation:

Better Record-Keeping

- Automatic digital records

- Clear transaction trails

- Easy to match with invoices

- Simplified year-end reporting

1099 Reporting

If you receive EDI payments as a contractor or freelancer:

- Track all EDI payment income

- Ensure payers have your correct tax information

- You may receive 1099-NEC forms for payments over $600

Sales Tax

For businesses collecting sales tax:

- EDI data can include tax amount breakdowns

- Easier reconciliation with sales tax reports

- Reduced errors in tax calculation

The Future of EDI Payments

Real-Time Payments

The Federal Reserve’s FedNow service and The Clearing House’s RTP network are expanding real-time payment capabilities, which may integrate with EDI data.

Enhanced Data Standards

Newer standards like ISO 20022 are being adopted, providing even richer payment data and better international compatibility.

Blockchain Integration

Some companies are exploring blockchain technology to create more transparent, immutable EDI payment records.

AI and Machine Learning

Artificial intelligence is being used to:

- Automatically categorize EDI payments

- Detect anomalies or fraud

- Predict cash flow based on EDI payment patterns

- Improve reconciliation accuracy

Frequently Asked Questions

Can I refuse an EDI payment?

Yes, but you’ll need to contact the sender and request an alternative payment method. However, many large companies require vendors to accept EDI payments.

Do EDI payments cost money to receive?

Most banks don’t charge fees to receive ACH EDI payments, but some business accounts may have transaction fees. Check with your bank.

How long do EDI payments take to process?

Standard ACH EDI payments typically take 1-2 business days. Same-day ACH is available for faster processing at a higher cost.

Can individuals receive EDI payments?

While EDI payments are primarily used in B2B transactions, individuals who work as contractors or freelancers can receive them through business accounts.

What’s the maximum amount for an EDI payment?

Standard ACH EDI payments have no maximum limit, though banks may have their own policies. Very large transactions might use wire transfer EDI instead.

Can EDI payments be reversed?

Yes, but only under specific circumstances like duplicate payments, incorrect amounts, or unauthorized transactions. Reversals must be initiated quickly.

Key Takeaways

- EDI payments are electronic transactions that include detailed payment data alongside the money transfer

- They’re safe and secure when processed through legitimate banking channels

- Common on bank statements for B2B payments, healthcare reimbursements, and government payments

- Always verify unexpected payments by checking your records and contacting the sender

- Beneficial for businesses due to automation, accuracy, and faster processing

- Require compatible systems to fully leverage the remittance data included

Conclusion

EDI payments represent the modern standard for business-to-business transactions in the United States. When you see an EDI payment on your bank statement, it’s typically a sign that you’re working with companies using efficient, automated payment systems.

While the term might seem technical at first, understanding EDI payments helps you better manage your finances, quickly identify incoming funds, and take advantage of the detailed transaction data these payments provide.

Whether you’re a freelancer receiving your first EDI payment from a corporate client or a small business owner considering implementing EDI for your own payables, knowing how these transactions work ensures you can navigate the modern payment landscape with confidence.

Remember to monitor your bank statements regularly, verify unfamiliar transactions, and don’t hesitate to contact your bank or the payment sender if anything seems amiss. With proper awareness and attention, EDI payments can significantly streamline your financial operations and improve your cash flow management.

![What Is FSUK Payment on Bank Statement (Sports Direct Frasers Group)[2026]](https://yourbankstatementconverter.com/blog/wp-content/uploads/2026/03/What-Is-FSUK-Payment-on-Bank-Statement-Sports-Direct-Frasers-Group2026-300x169.jpg)

![What Does CR Mean on a Bank Statement (Credit Explained)[2026]](https://yourbankstatementconverter.com/blog/wp-content/uploads/2026/03/What-Does-CR-Mean-on-a-Bank-Statement-Credit-Explained2026-300x169.jpg)

![What Does BP Mean on a Bank Statement (Both Meanings Explained)[2026]](https://yourbankstatementconverter.com/blog/wp-content/uploads/2026/03/What-Does-BP-Mean-on-a-Bank-Statement-Both-Meanings-Explained2026-1-300x169.jpg)