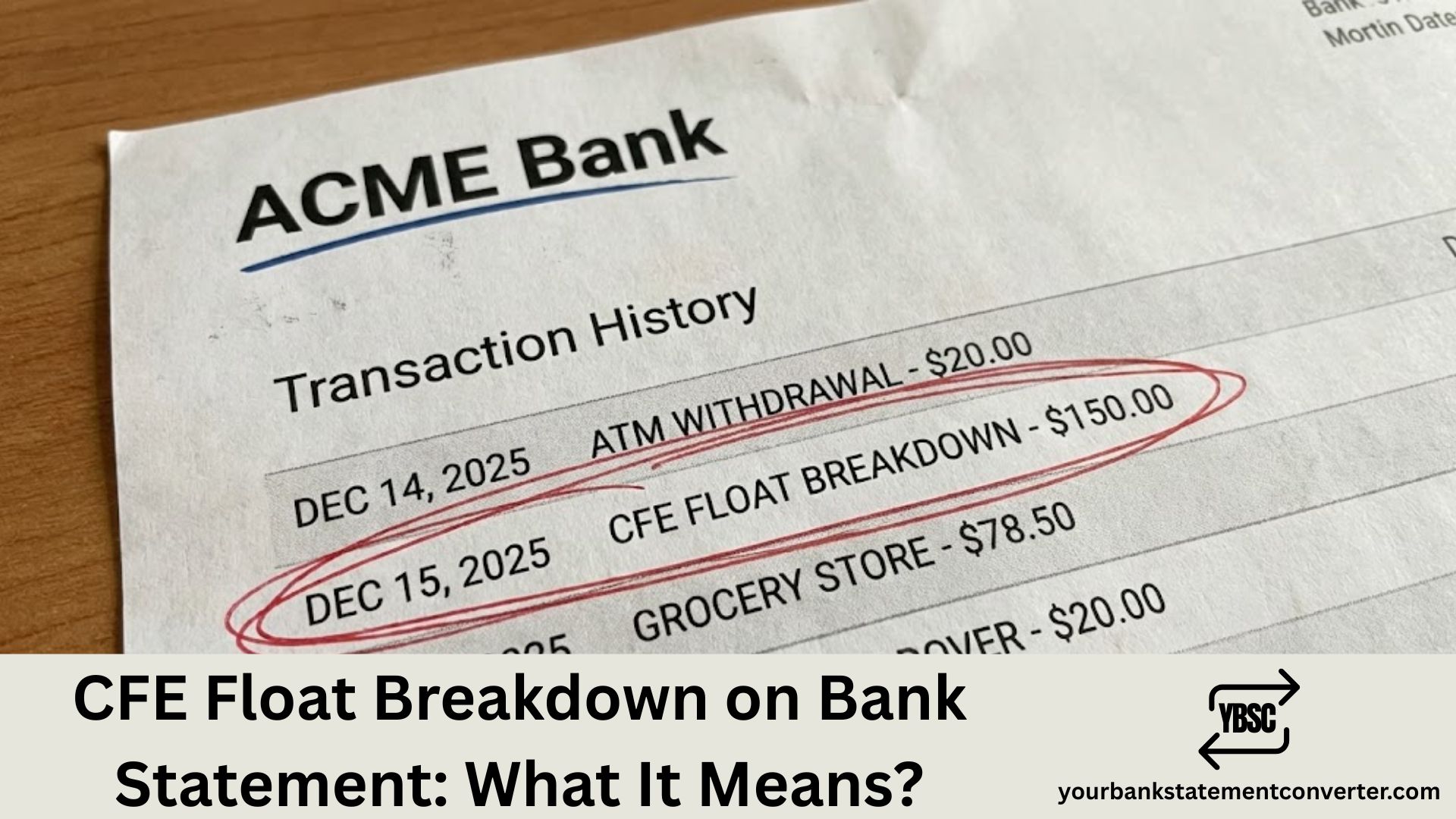

Noticed a “CFE Float Breakdown” entry on your bank statement and wondering what it means? You’re not alone. This term confuses many account holders, especially those banking with credit unions. Here’s a quick explanation to help you understand exactly what you’re looking at.

What Is CFE Float Breakdown on My Bank Statement?

CFE Float Breakdown refers to how your financial institution itemizes funds that are in transit or pending clearance in your account. CFE typically stands for credit unions like Central Florida Educators Federal Credit Union (now Addition Financial) or similar institutions.

The “float breakdown” section shows you:

- Deposited checks awaiting clearance – Checks you’ve deposited that haven’t fully processed yet

- Pending deposits – Funds credited to your account but not yet available for withdrawal

- Collection float – Money showing in your account that the bank hasn’t actually received from the paying institution

- Disbursement float – Payments you’ve made that haven’t cleared your account yet

When you deposit a check, the bank credits your account but places a hold until the funds clear from the issuing bank. This hold period—typically 1-3 business days for most checks—is your float period.

Why Does Float Appear on Your Statement?

Banks show float breakdowns to help you understand the difference between your current balance (total funds credited) and your available balance (funds you can actually spend). Under the Expedited Funds Availability Act (Regulation CC), financial institutions must disclose their funds availability policies and notify you when holds are placed.

How Long Do Funds Stay in Float?

| Deposit Type | Typical Availability |

|---|---|

| Cash deposits | Same day |

| Direct deposits | Same day |

| Government checks | Next business day |

| Personal checks | 2 business days |

| Large deposits ($5,525+) | Up to 7 business days |

How to Track Float in Your Bank Statements

Managing your float effectively requires understanding both balances on your statement. If you regularly reconcile bank statements—whether for personal budgeting or business accounting—tracking float helps prevent overdrafts and bounced payments.

For accountants, bookkeepers, and small business owners who need to convert PDF bank statements into workable formats, tools like Your Bank Statement Converter simplify this process. Converting your statements to Excel makes it easier to track pending transactions and reconcile your actual available funds.

Common Questions About CFE Float

Is float the same as a hold?

Yes, essentially. Float refers to funds in limbo during processing, while a hold is the bank’s action preventing access to those funds.

Can I spend money that’s in float?

No. Attempting to withdraw or spend float funds before they clear can result in overdraft fees or returned payments.

Why did my check take longer than expected to clear?

Large deposits, new accounts, previously bounced checks, or suspected fraud can extend hold times beyond the standard 2-day period.

Understanding CFE Float Breakdown: Key Takeaways

The CFE Float Breakdown on your bank statement simply shows you which deposited funds are still processing. It helps you understand why your available balance differs from your total balance. Always check both balances before making large purchases or payments to avoid insufficient funds fees.

If you need to analyze your bank statements for accounting purposes or reconcile your books efficiently, converting your PDF statements to Excel format saves significant time. Your Bank Statement Converter handles this conversion quickly, making float tracking and financial reconciliation straightforward.

FAQs

What does float mean on a credit union statement?

Float on a credit union statement represents funds that have been deposited but aren’t yet available for withdrawal because they’re still being processed or verified by the issuing bank.

How do I know when my float funds will be available?

Check your deposit receipt or online banking portal for the funds availability date. Most banks also send notifications when holds are placed on deposits.

Does CFE only appear on credit union statements?

CFE typically appears on statements from credit unions (like Central Florida Educators FCU), but similar float breakdowns appear on bank statements using different terminology like “pending deposits” or “uncollected funds.”

Can float affect my ability to pay bills?

Yes. If you schedule payments based on your total balance rather than available balance, those payments may bounce if the float funds haven’t cleared yet.

Why is my available balance lower than my account balance?

The difference usually represents your float—deposited funds still being processed—plus any authorized transactions that haven’t posted yet.